With the stock market recently hitting new all-time highs again, times are exciting for people who are fully invested, but these conditions can be more frustrating for those who have cash available to put to work. Higher stock prices do make it a bit tougher for bargain hunters to find deals, but stocks don’t all rise or fall on a synchronized schedule. Some invariably lag behind those broad-market patterns.

The tough part of seeking out bargains among those laggard stocks is that there’s usually a good reason why a company’s shares didn’t participate in the rally. Still, even when there’s a good reason, at the right prices, out-of-favor stocks may well be worth buying.

With that in mind, three Motley Fool contributors went looking for stocks the recent bull market has left behind that might have a bit of life ahead of them, despite Wall Street’s pessimism. They came up with Pfizer (NYSE: PFE), Confluent (NASDAQ: CFLT), and Kinder Morgan (NYSE: KMI). But only you can decide whether they’re cheap enough to be worth a spot in your portfolio.

A mighty drug maker brought low by the market

Eric Volkman (Pfizer): With rare exceptions, star power rarely lasts forever. One example of a company that recently experienced the downside of this dynamic is pharmaceutical giant Pfizer.

A few years ago, Pfizer was a hot item thanks to its heavy involvement in the fight against COVID-19. It was the co-developer of the go-to coronavirus vaccine Comirnaty. On top of that, it is the company behind the well-known COVID antiviral treatment Paxlovid.

In the thick of the pandemic, when hundreds of millions of people were eager to get inoculated, and when treatments for the disease were in high demand, Pfizer experienced big leaps in revenue and profitability.

Even the mightiest company would find it challenging to follow up that sort of performance with a similar second act, and Pfizer is falling short in the minds of many. After all, both its recently released fourth-quarter and full-year 2023 headline figures were down substantially as the pandemic has evolved into an endemic and the public health crisis has receded. Revenue for Q4 and the full year fell by more than 40% on a year-over-year basis, with non-GAAP (adjusted) net income nose-diving by 91% in the quarter.

Yet those fourth-quarter figures beat the collective estimates from analysts, who were expecting the pharmaceutical giant to post a fairly deep adjusted net loss. Much of the upside surprise was due to Comirnaty, which is still making its way into the arms of people who are aware that COVID-19 remains a threat.

However, sales of several of Pfizer’s top products fell, compounding the generally bearish reaction to the earnings report. For example, in the face of intensifying competition, cancer treatment Ibrance saw a nearly 13% year-over-year decline in sales. Looming patent expirations for Ibrance and other top sellers are also making investors fret.

They really shouldn’t. Pfizer still has a solid lineup of blockbuster drugs, and it has a robust pipeline with potential blockbusters in development.

Meanwhile, its valuations look sickly, and will surely improve once the market gets past the idea that the company can’t sufficiently recover from the decline in its COVID-related revenues.

Its forward P/E is barely over 12, and its trailing price-to-sales ratio is a feeble 2.3. I don’t think it will continue to trade at such bargain levels for long. Strengthening the buy case is the company’s dividend, one of the most steady and reliable in the healthcare sector. At the current share price, it yields more than 6% — sky-high for a once and future blue chip stock.

Don’t call it a comeback

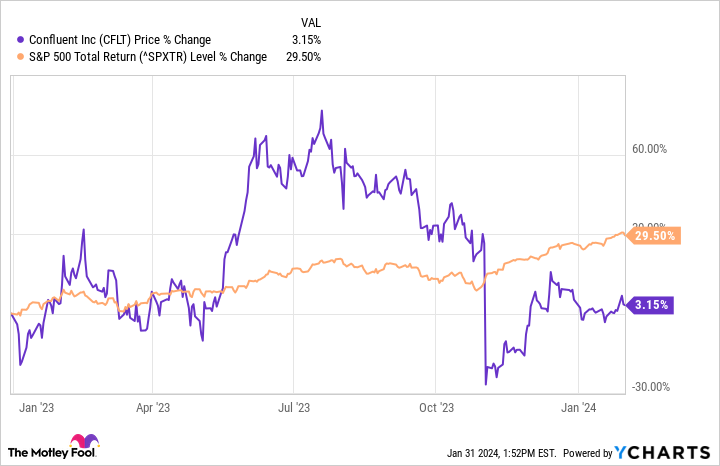

Jason Hall (Confluent): One look at the chart below may make investors think that Confluent is in trouble.

From its early 2023 low to its high point, Confluent’s stock price doubled, but then headed lower again before tumbling sharply back past that prior low when it reported third-quarter results in November.

What sent its shares tumbling? Frankly, the usual volatility of being a younger, still-developing business. Confluent is a leader in data streaming, and investors are focused on its growth rates and customer expansion. When it reported some churn with a few big customers that would carry over into early 2024, the market kind of freaked out.

My analysis says this was an overreaction. Confluent’s growth story remains intact.

Revenue was up 32% in the third quarter, and Confluent Cloud revenue was up 61%. Its growth has slowed, and investors expect to hear that it slowed further to 22% and 43% in the fourth quarter. (The company will report results for that period on Wednesday.) But Confluent Cloud (its version of Kafka built to live in AWS, Azure, etc) is still expected to grow by more than 40% per year.

Customer growth is still in the high-teens percentages, and the number of customers spending $100,000 or more with it annually is growing even faster. As a result, margins are improving and cash flows are getting stronger. The company forecast that it would be free-cash-flow breakeven in the fourth quarter, and expects to start generating positive free cash flow in 2024.

So while the market sees risk, I see a company that’s getting stronger and safer with each passing quarter. Now’s the time to buy this upstart in the brave new world of how businesses manage and use data.

This company’s industry still has decades of life left in it

Chuck Saletta (Kinder Morgan): Oil and natural gas may not be the sexiest forms of energy these days, but they remain in strong demand throughout the world. Indeed, according to the U.S. Energy Information Administration’s most recent Annual Energy Outlook, oil and natural gas use is expected to stay approximately stable between now and 2050.

Beyond that, it’s not too far a stretch to project beyond 2050 and presume that even if our supplies of greener energy continue to grow, it will still take a long time after that to completely eliminate oil and natural gas from the world’s energy mix. After all, you can’t really go from about 20 million barrels of oil per day and 30 trillion cubic feet of natural gas use per year to absolutely nothing overnight.

In addition, even if you do factor in a decline in oil and natural gas use over the very long haul, pipeline companies like Kinder Morgan are likely to be among the longest-lasting parts of the industry. Pipelines have high up-front costs to build, but they benefit from relatively low costs per barrel of oil or cubic foot of natural gas to transport that energy.

As a result, as long as oil and natural gas are needed and have to move from where they’re produced to where they’re processed and consumed, pipelines will still be needed to move them around. Other transportation methods — like trucks and trains — will likely see their use for oil and natural gas transportation drop before pipelines do.

Despite those decent prospects for decades to come, Kinder Morgan’s shares have basically gone nowhere for more than five years, even as its dividends have continued to recover. Its market capitalization is around $38 billion, and it generated around $5.6 billion in cash from operations over the past 12 months. At that valuation — less than 7 times its cash-generating ability — the market is virtually giving up on the company, despite those solid decades likely ahead of it.

Kinder Morgan may not be the fastest-growing company on the planet, but given its prospects, its shares certainly look cheap enough to be worth considering at the moment.

Get started now

Although the market does occasionally leave solid companies behind when it rallies, true bargains rarely remain bargains for long. That’s why now is the time to take a look for yourself and see if you think these businesses’ shares are worth picking up at their current prices. Even if the market doesn’t end up bidding them up for big rallies, you just might find yourself with stocks of quality companies you’ll be pleased to hold onto for many years to come.

Should you invest $1,000 in Pfizer right now?

Before you buy stock in Pfizer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Pfizer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of January 29, 2024

Chuck Saletta has positions in Kinder Morgan and Pfizer and has the following options: long January 2026 $25 calls on Pfizer, short January 2026 $25 puts on Pfizer, short March 2024 $22.50 puts on Pfizer, and short March 2024 $27.50 calls on Pfizer. Eric Volkman has no position in any of the stocks mentioned. Jason Hall has positions in Confluent. The Motley Fool has positions in and recommends Confluent, Kinder Morgan, and Pfizer. The Motley Fool has a disclosure policy.

The Bull Market Left These 3 Stocks Behind, but They’re Buys Right Now was originally published by The Motley Fool